[ad_1]

I don’t get a lot of readers asking for currency exchange tips on this blog or in my social media feeds, but I do get a lot of questions about travel money from friends and relatives. While experienced travelers mostly default to using ATMs and credit cards, less frequent vacationers have a lot of questions about foreign currency before they go traveling.

I’m currently traveling around Europe and I have five currencies in various pockets and wallets in different places. Some from previous travels, some from a country I’m returning to, and some I got from someone who had just left a place I am headed to in June.

Euros, dollars, lev, lek, and a few leftover Mexican pesos in case you were wondering.

That’s not common though: normally you want to spend all you have in one currency before moving on to the next place or heading home. More on that later, but let’s start at the beginning of the journey with these currency exchange tips.

Maybe Get Foreign Currency Locally Before Leaving (but not a lot…)

Although it’s generally not a good idea to load up on currency before you leave, despite what your friendly tour operator may tell you, it gives a lot of people peace of mind to have some local cash in their pocket when they touch down.

In general, the more your own city is visited by foreigners, the more currency exchange options you’ll have. Where I live in Mexico, options are quite limited. When I’m at the Mexico City airport, however, I could change dollars or pesos for all kinds of currencies if I wanted to have cash on hand upon arrival. If you’re Australian, you can use a place like Crown Currency Exchange in Brisbane or find dozens of options scattered around in most European cities.

In most cases, however, the exchange rate you’ll get at these places is nowhere close to the official bank rate. These exchange places are businesses, after all, and they make money on the spread between the actual rate and what you’re willing to take in exchange. They earn a profit from every transaction.

You’ll probably get an even worse rate at your bank, but this is not consistent so it’s worth a check. Ideally have an app on your phone that gives you the current market rate so you can compare and see how much you are sacrificing for convenience. I use the app from xe.com and I can save the currencies I want to keep tabs on, switching them out as travel plans change.

Ask Around About Leftover Cash

If you know a friend of yours recently went to a foreign country you’re headed to, it’s worth asking them if they have any leftover cash. If they do, they’ll likely be glad to offer it to you at the current market exchange rate.

Or if you belong to some kind of local message board or travelers club, put it out there where you’re headed to and you might get a response. This is especially fruitful in expat areas since there are bound to be many nomads in that group. Some of them are probably sitting on foreign cash they’d like to unload if they don’t have plans to return to that country.

Get Your Debit Card(s) Sorted to Reduce Foreign ATM Fees

Many experienced travelers will tell you that an article about currency exchange tips should only be a one-item listicle: “always use a debit card at ATM machines.” That’s because in almost every country in the world, you’ll get a better rate taking money out of a bank ATM than you will by any other method—assuming you don’t do it wrong.

Doing it wrong can take several forms on site, which I’ll get to in a minute, but you can also do it wrong if you’re handing over far more in fees than you have to. If your bank charges you $6 every time you take out money, on top of what the local bank is also charging, you could be paying several percentage points in fees each time you make a withdrawal. That can really add up.

The way to keep these fees to a minimum is to get a card that doesn’t charge you an ATM fee or better yet, doesn’t charge you and reimburses the local charges. The former options include cards with a big network that allow you to take money out of their own international locations, like with HSBC, Scotiabank, or Citibank. Some let you take money out of any ATM connected to the Plus network with no fees.

A better option can be the ones from the likes of Capital One that don’t charge you no matter what machine you use. My wife has the Capital One 360 card attached to her checking account and never pays a fee to them.

To take it a step further and get out of the local fees too, get a premium debit card attached to a cash account of Schwab, Fidelity, or a customer-focused credit union. These will not only avoid charging you on their end, but they’ll also give you back the fee that the local bank charged, which can be several dollars each time you try to get to your own money.

There’s usually a monthly limit, but that’s eight a month with my Fidelity one I think. I’m not sure because I’ve never tapped it enough times in one month for it to matter.

Just Say No to Foreign Transaction Fees

If your credit card hits you with a foreign transaction fee, this is a card you should vow to never use again outside of your home country. Switch it out for one that’s not trying to pickpocket you when you travel.

There’s no excuse for this fee. It’s a pure, unadulterated money grab from a greedy corporation, mostly extracted from people who don’t know any better and don’t look for a better deal. The company is already making money in several other ways, including from the merchant and on the currency spread, before we even get to annual fees and high interest charges. So you are voluntarily handing them your hard-earned money if you pay this.

Surprisingly, you even see this customer robbery with travel cards, the ones branded by airlines like American or Southwest, or by hotel chains that you would think want you to use their card when you travel. Ones that do not charge a foreign transaction fee usually tout this in their benefits (even though not stealing from you shouldn’t be listed as a benefit, it should be a given).

See these posts of mine on credit cards that earn free flights and ones that get you free hotel nights and I believe all but the Southwest one don’t charge an extra fee. My Wyndham one via Barclays doesn’t either, nor does the Barclay AA one—just the Citi versions.

Assuming you’ve eliminated that, credit cards will usually give you a favorable exchange rate that’s better than what you would get on the street. So don’t hesitate to use plastic.

Be Aware of Rare Exchange Exceptions

I mentioned before that there are a few places in the world where the normal rules of always using an ATM don’t apply. As I write this, one is Argentina, where the official rate is nowhere close to the street rate, locally called the blue rate, that you should really be getting for your dollars or euros. See more details here on bringing cash to Argentina.

They are not the only country with high inflation though and whenever there’s super-high inflation, the street rate will be updated more often than the bank rate. Sometimes several times a day. So you could get a better rate at a money exchange place in Istanbul than you get with your debit card, though it probably won’t be huge.

The only other exception I’ve run into around the world is the Czech Republic, which now wants to be called Chechia. Besides all the scammy exchange places in the center that are out to rob you, the other disturbingly odd trend I found there was that ATMs were giving a rate that was 10% less than the market bank rate. This is a huge spread and I found it at three different bank chains’ ATMs.

I’ll be back in July and will see if that’s still the case. I may hang onto some euros so that I’ve got options if so. I’ll also use my credit card more as the rate was much closer to the market rate for those charges.

Exchanging Money at the Airport

Although it would be logical to expect airport exchange kiosks to have a favorable exchange rate, that’s often not the case. Plus sometimes they pull sneaky moves to keep you from figuring out the real rate, like listing how much you get for changing $250 instead of listing how much you get for $1. They want to make you do tricky math and hopefully give up trying to figure it out.

In general, competition brings down prices so if you see 20 exchange booths like I’ve seen in some airports, the rate is probably good. If you only see a monopoly of one, probably not. Again, have an exchange rate app on your phone and refresh it well before you land in case you don’t have service in the airport when you land.

I can’t remember the last time I landed in a city and had trouble finding an ATM though, either at the airport or near where I’m staying. The only time I use the airport exchange booths is when I have a sizeable amount of money left over at the end I won’t use anytime soon, like when I traded in Swiss francs for euros at the Geneva airport.

Avoid ATM Tricks and Scams

I wish I could say that you could use any ATM in the world and expect the same outcome, but unfortunately, that’s not the case. Who knows how many millions of dollars are lost to fraud each year, then there are millions more lost to onerous fees that are legal but dishonest.

On the fraud side, you have to be aware that there’s such a thing as an “ATM skimmer.” That is a fake slot meant to steal your card info. This can take two forms. the first is a fully fake ATM that is only set up to steal your card info. The more common method is a skimmer that has been attached to a real ATM by a criminal to accomplish the same thing.

I’ve never experienced this personally, but I do try to be careful, so here’s my advice on that.

First, does the ATM reader look or feel funky? Sometimes the skimmer is slid in on top of the real slot, so if there’s an extra protuberance that’s a clear warning, or if you grab it and it moves, that’s a bad sign. Move on and if you’re feeling generous, notifiy the bank or put a warning on Google Maps.

One rule of thumb I try to stick by is to use ATMs that are attached to a real bank that customers walk into, rather than little boxy ATMS sitting by themselves by the side of a street. In cities this is usually easy to do. It’s not so easy at airports, however, so sometimes you have to take a leap of faith there and use a kiosk version. Or when you’re in a supermarket and there are four or five of them lined up.

ATM Fee Differences and the “Accept Conversion” Scam

When possible, try to use one affiliated with an actual bank, not one from Euronet or some other fee-happy operation. Sometimes you’ll find that the fee for one machine can be 2X or 3X times the fee for the one right next to it. You see this in Mexico often where Banorte charges the equivalent of $7 or $8 where others are only a buck or two.

There’s often no law about how much these banks can charge you so they’ll try to charge as much as they can get away with. You’re not a real customer so they don’t care what you think. They got your money then you buzzed off.

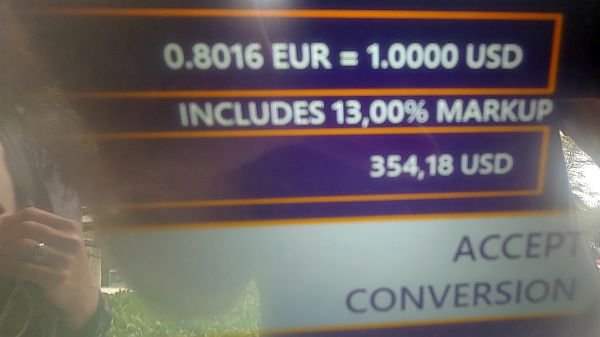

The other way they get a big payoff is also legal, but very sneaky. It’s called the “Accept Conversion Scam” and it’s becoming more and more common. Basically, when you take out ATM money or charge something to a credit card, the merchant can charge you in the local currency or charge you in your home currency. The first is what you want, the second is what they want.

The way it works in practice is that you’ll get to one of the last screens as you move through the ATM options and a screen will pop up with what seems like an obvious choice: on one side will be “Accept Conversion” or “Continue With Conversion.” On the other side will be “Deny Conversion”or “Continue Without Conversion.”

Always choose the negative: you do not want to accept this conversion. This sounds tricky because it is, intentionally. The bank wants to fool you into accepting the worse rate and if you do, you basically hand them a few bills and they laugh heartily as they light up their cigars. Here’s how much of a difference it makes. I took this photo today in Europe but I’ve seen it all over.

The real exchange rate should be 0.91 to the euro, not 0.80. As they say on the screen if you’re paying attention, they’re padding their profits with a 13% markup. At your expense.

Other Currency Exchange Tips

There are a few more random tips that don’t require a whole section so I’m going to list them here. That way I can add on later if I forgot something that one of you readers points out.

– You need a travel money and banking back-up plan, hopefully with multiple redundancies and “what if” scenario solutions. You want to leave with more than one debit card, more than one credit card, and copies of your info available by online banking and apps. You want cards stored in at least two places on your person and in your luggage and if there are two of you, take advantage of that for more back-ups.

– Since your phone payment system is usually connected to a bank account or credit card, tapping your phone is the same as tapping a card and can therefore reduce the amount of cash you’re carrying around.

– Be advised though that some countries are very cash-oriented so if you don’t have any in your pocket you’re going to face a lot of uncomfortable situations. This is especially true once you get outside of the most developed countries and it extends across nearly every continent, including Europe.

– Don’t forget that it’s very hard to tip a service provider if you don’t have cash. In some countries they don’t even have a way to add it to the bill if you pay by credit card either, like in a restaurant or bar. Locals leave the tip part in cash. Don’t be that guy or gal who always needs someone else to spot them.

– As mentioned earlier, ideally you want to spend all your cash before leaving and hopefully it’s not on overpriced duty-free items. But if you’re stuck, you can take a loss at the currency exchange counter or there’s probably someone who could use a gift from you…

[ad_2]